Got Leftover 529 Money? Here’s What You Can Do With It

What happens if you or your kids don’t use all the money in a 529 college savings plan? One caller recently asked this on our show. His grandparents had started a 529 for him, but after earning his associate’s degree, he dropped out. He still had about $13,000 sitting in the account and wasn’t sure what to do with it.

If you’re in a similar situation, you might feel like your money is stuck. After all, 529s are designed for education expenses. But the good news is that there are several smart ways to put that money to work.

1. Pay Down Student Loans

You can use up to $10,000 in lifetime benefits per person from a 529 plan to pay off student loan debt. If you have loans, this could be a smart first move.

For example, if your loan balance is $20,000 at 6% interest, applying $10,000 from a 529 could save roughly $600 per year in interest and thousands over the life of the loan.

💡 Pro Tip: Even if you already used loans to pay tuition or housing, you can reimburse yourself with 529 funds, as long as you have proper documentation. Keep tuition statements, rent receipts, or invoices for books and supplies. The IRS allows reimbursement years later, provided you can prove the expenses.

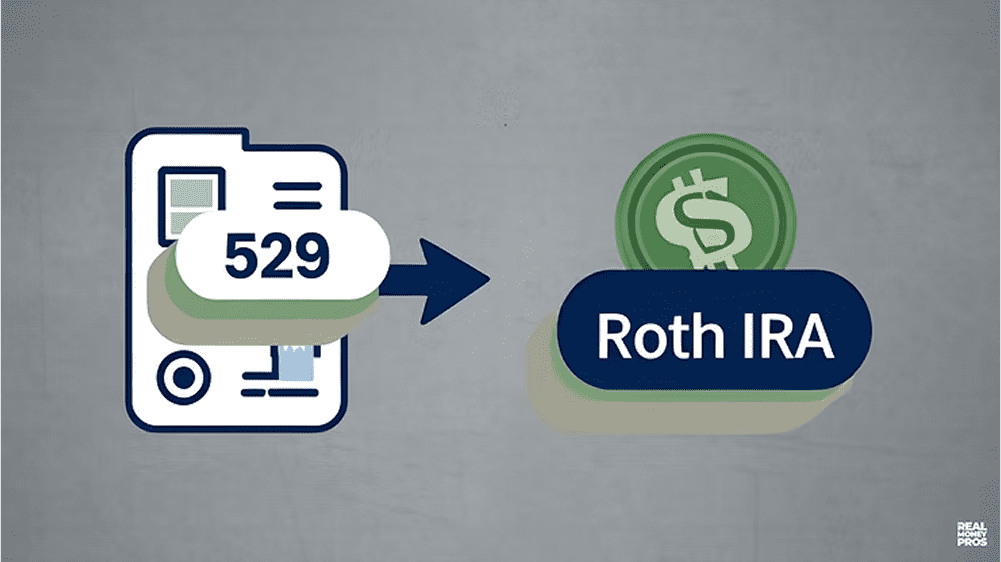

2. Roll Over Into a Roth IRA

Recent rule changes now allow you to roll leftover 529 funds into a Roth IRA. This is a game-changer because it lets you turn education savings into retirement savings.

Here’s how it works:

- The 529 must have been open for at least 15 years.

- The beneficiary must have earned income.

- Rollovers count toward the annual Roth IRA contribution limit (currently $7,000 for most people).

- There is a lifetime rollover limit of $35,000 per beneficiary.

In practice, you could rollover up to $35,000 into your Roth IRA over time. You could also change the 529’s beneficiary, and if there are leftover funds, the new beneficiary could use the rollover option, following the same rules. Keep in mind that normal annual contribution limits and the five-year rule for Roth contributions still apply. And this leads us to the next option...

3. Change the Beneficiary

If you don’t need the money yourself, you can transfer the 529 to another eligible family member, such as:

- A sibling or cousin

- A spouse

- Your own children in the future

This flexibility makes 529s a generational tool. Families with multiple children or grandchildren can keep the money working for education rather than letting it sit idle.

4. Take It Out (as a Last Resort)

You can always withdraw the money, but there’s a catch. Any earnings (not your original contributions) are taxed as ordinary income and subject to a 10% penalty if not used for qualified education expenses.

For example, if your $13,000 balance includes $3,000 in earnings, cashing out could cost you $300 in penalties plus taxes on the $3,000. This makes withdrawal the least attractive option, so consider it only if the others aren’t feasible.

The Big Takeaway

Leftover 529 funds aren’t a problem—they’re an opportunity. With the right moves, you can:

- Reduce student debt faster

- Boost retirement savings

- Support another family member’s education

The key is knowing your options and keeping thorough records.

Want More Real-World Money Advice?

If you want guidance on 529s or other financial questions, contact us to connect with an advisor!