The Boring (and Time-Tested) Way to Become a Millionaire

The Millionaire Myth

According to Fidelity’s Q4 2024 Retirement Analysis, the number of 401(k) millionaires is at an all-time high. These aren’t hedge fund managers or Silicon Valley unicorn founders. They’re regular people with jobs, bills, families—and a plan. They automated their savings, invested regularly, and gave it time. Boring, right?

Automation: Your Secret Weapon

The most powerful wealth-building move you can make is also one of the easiest: automate your retirement contributions.

By setting up payroll deductions into a 401(k) or IRA, you’re putting your savings on autopilot. That removes the temptation to spend it, the need to remember to transfer it, and the

danger of waiting for the “perfect” time to invest.

And if your employer offers a match? That’s an immediate boost—before your money even hits the market. For example, let’s say you earn $60,000 a year and contribute 6% of your salary ($3,600/year) to your 401(k). If your employer matches 100% up to 6%, that’s another $3,600 added to your account—instantly doubling your contribution. You’re already at $7,200 a year without lifting a finger beyond enrolling.

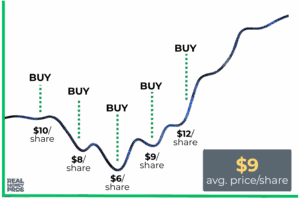

Dollar-Cost Averaging: A Built-In Advantage

This helps in two major ways:

- You buy more shares when prices are low—which may boost your long-term gains.

- You avoid trying to time the market—which almost no one does successfully.

Over time, this strategy helps smooth out the volatility. It keeps you consistent and less reactive, even when headlines scream panic.

This hypothetical illustration is for educational purposes only and

does not reflect actual performance.

Time Beats Timing

The people who reach that million-dollar milestone didn’t get there by being perfect investors. They did it by starting early and sticking with the plan—even through market noise.

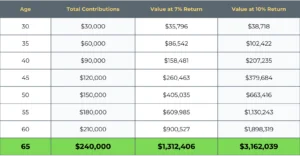

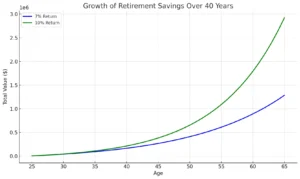

Let’s run a simple example: A 25-year-old who invests $500 per month into a retirement account that averages a 7% annual return will have over $1.3 million by age 65. That’s without needing to time the market—just consistency and time (though a thought-out investment strategy helps tremendously).

Now, imagine that same person earns a 10% average return instead (which is close to the historical average of the S&P 500, before adjusting for inflation). Their nest egg at 65 grows to over $3.1 million. That’s the power of compounding over 40 years.

This hypothetical illustration is for educational purposes only

and does not reflect actual performance.

You don’t need to pick the perfect stock or time the market—you just need consistency, patience, and time. And if you earn a slightly higher return (which a well-diversified portfolio can help support), the impact can be huge.

This hypothetical illustration is for educational purposes only and

does not reflect actual performance.

And as your income grows, your contributions should too. This is where many people fall into the trap of lifestyle creep—spending more as they earn more. But if you make it a habit to increase your savings rate along with your income—even just 1% of your earnings at a time—you’re harnessing your raises to accelerate your financial future instead of letting them is appear into bigger car payments and nicer dinners.

Starting Late? You Still Have Power

Here’s why you still have plenty of power:

- Your earning years are often at their peak now. You likely have more disposable income than in your 20s or 30s—so you can save more each month.

- Catch-up contributions can turbocharge your savings. If you’re 50 or older, you can contribute an additional $7,500 per year to your 401(k), on top of the standard limit. Recently implemented within SECURE Act 2.0, people age 60–63 can contribute even more, up to $11,250 in catch-up contributions. What a boost!

- Time still matters—even 10 or 15 years can make a big difference. Compound interest may take longer to show its impact, but every dollar you save now has the potential to grow exponentially over time.

- Smart investing and controlling expenses can accelerate growth. Choosing a diversified portfolio that fits your risk tolerance and avoiding early withdrawals keeps your plan on track.

Stay the Course

The market will have bad days, bad quarters, even bad years. That’s normal. Historically, the U.S. stock market has always recovered from downturns. Whether it was the dot-com bubble, the 2008 financial crisis, or the COVID-19 crash, the market has historically bounced back—and those who stayed invested had often come out stronger on the other side.

Past performance is not indicative of future results. This image

is for illustrative purposes only and does not represent a specific investment recommendation.

In fact, the people who tend to build the most wealth over time aren’t the ones who perfectly timed the market. They’re the ones who didn’t flinch when things got rough.

When the market drops, prices are essentially on sale. Stocks you believe in may be cheaper than they were yesterday. If you’re consistently contributing to your retirement or investment accounts, this is when your dollars can go further—potentially buying more shares for the same amount of money. This is the essence of dollar-cost averaging: investing a set amount regularly, regardless of market conditions. It helps smooth out the impact of volatility over time, and during downturns, it can enhance your long-term gains.

Let’s say you’re investing $500 a month, and the market drops 20%. That $500 now buys more shares than it did the month before. If the market recovers—and historically, it has—you’re potentially in a better position because you own more of the asset at a lower average cost.

Avoid These Common Mistakes

These are the mistakes that quietly eat away at your progress—and they’re all avoidable:

- Skipping your employer match: Not contributing enough to get the full match is like turning down a raise. If your employer offers to match 3% or 6% of your salary and you’re not taking advantage, you’re walking away from thousands of free dollars each year.

- Stopping contributions during market downturns: It feels safe, but it can work against you. You miss out on buying low—and when you finally feel comfortable again, prices may be higher. Stick with it through the dips; it’s part of the process.

- Cashing out your 401(k) when changing jobs: This one can be costly. Not only do you lose years of potential growth, but you’ll owe taxes and possibly early withdrawal penalties too. Instead, roll it over into a new 401(k) or an IRA—keep your money working for you.

- Letting lifestyle creep outrun your savings: It’s easy to justify spending more as you earn more. But make it a rule: with every raise, increase your retirement contribution first. That keeps your savings on pace with your income—and your future self will thank you.

Final Thoughts

Building real wealth doesn’t require complexity. It requires discipline, a system, and time. You don’t need to “outsmart” the market—you just need to outlast it.

In our office, we’re big fans of the boring path—the one with automatic deposits, rising contributions, and long-term perspective. For many investors, it works! If you’re not sure your retirement strategy is on the right track—or want help building one that fits your lifestyle and goals—we’re here to help.