The Disconnect Between Portfolio Growth and Real Income

There’s a shift that tends to happen when markets perform well.

It doesn’t feel like a problem. In most cases, it feels like progress.

Account values rise and your account statements look better. The quiet concern that used to sit in the background—Am I going to be okay?—starts to fade.

And as that concern fades, something else begins to change: Your behavior.

The Shift Most People Don’t Notice

For many investors approaching retirement, the primary focus isn’t growth—it’s income.

The questions are familiar:

- How will I replace my paycheck?

- Will my assets support my lifestyle?

- Do I have enough to make this work long term?

Those questions don’t just disappear, but strong market performance can make it feel like they have.

And that’s where the shift begins… Not in the portfolio itself, but in how the portfolio is perceived.

When Growth Starts Driving Decisions

As account values increase, confidence tends to rise alongside them.

Spending decisions feel easier.

Larger purchases feel more justified.

Things that once felt discretionary start to feel reasonable.

None of that is inherently wrong!

The issue shows up when those decisions become tied to account values that haven’t been translated into something stable or repeatable.

The lifestyle begins to adjust to reflect growth before that growth has been structured into a plan.

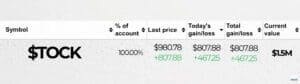

Consider an investor with a growth-oriented position that’s performed well over the past year or two. The account looks strong. They delay a planning conversation, make a few larger purchases, and tell themselves, this is working.

But the underlying question hasn’t changed: How does this eventually turn into sustainable income when I need it?

Growth Doesn’t Equal Income. Structure Does.

One of the most common disconnects we see is this: A portfolio grows significantly, but the structure behind it remains unchanged.

A portfolio heavily weighted toward growth assets may increase in value while producing very little actual cash flow.

That creates a mismatch:

- The account looks strong

- Confidence increases

- But the ability to generate reliable income is still uncertain

At some point, those need to align because growth alone doesn’t fund retirement. A structured plan does.

Where the Risk Actually Shows Up

The risk here usually isn’t the investment itself. It’s the gap between what the portfolio is doing and what it’s expected to support.

When that gap widens, planning tends to get pushed out. And the longer it’s delayed, the more reactive decisions become—especially if market conditions change.

This is where many investors unintentionally shift from being proactive to reactive, without realizing it.

What Disciplined Investors Do Differently

This isn’t about trying to call a market top or predict short-term movements.

It’s about recognizing when conditions have changed and responding with intention.

During periods of strong performance, more disciplined investors tend to:

- Revisit the purpose of their portfolio

- Evaluate how gains can support long-term objectives

- Consider repositioning a portion of those gains

- Make sure future income needs are still being addressed

They don’t eliminate growth, they make sure the strategy evolves along with the results.

Bringing the Plan Back Into Focus

Market performance can create opportunity, but it can also create distraction from reality.

The goal is to ensure that progress in the portfolio translates into progress toward income.

That may involve:

- Clarifying future income needs

- Evaluating whether current investments actually support those needs

- Making gradual, intentional adjustments over time

None of this requires drastic action, but it does require attention.

Final Thought

Strong market performance can feel like validation.

And in many cases, it is. But it doesn’t replace the need for a plan.

Because over time, the objective shifts. It’s no longer just about growing the account. It’s about making sure what you’ve built can actually support what comes next.

Next Step

If recent market performance has changed how your portfolio looks—or how you feel about it—it may be worth stepping back and asking a more specific question:

Has your income plan kept pace with your portfolio’s growth?

Our team at the Real Money Pros and Apollon Wealth Management can help you connect those pieces and evaluate whether any adjustments may make sense based on your goals.

Use the “Find an Advisor” tab on our website to get connected today!