Stock Compensation Tax Planning: RSUs, Stock Options & ESPP Mistakes

For many high earners, stock compensation feels like a sign that things are going well. And often, it is.

Restricted stock units. Employee stock purchase plans. Stock options. These benefits can be powerful wealth-building tools — particularly for executives, key employees, and professionals at thriving companies. But they can also introduce a level of financial complexity that quietly catches people off guard.

Because while stock compensation may feel like “extra upside,” the tax consequences, timing decisions, and portfolio risks behind it are rarely as simple as they appear. And when planning doesn’t keep pace, the surprises can get expensive.

A Situation We See More Often Than You Might Think

Picture a senior employee earning $450,000 a year. They receive quarterly RSU vesting, participate in their company’s ESPP, and have built up a meaningful amount of employer stock over time.

On paper, things look great. Income is strong, net worth is growing, and the company stock has performed well.

But beneath the surface, a few risks may be quietly building. Employer stock has grown to a disproportionate share of their portfolio. Tax withholding tied to stock compensation may not fully reflect their actual liability. And decisions around holding, selling, or exercising are being made without a broader strategy connecting them.

Then tax season arrives — and what felt like a wealth-building opportunity suddenly feels a lot more complicated. This happens more often than most high earners expect.

The 4 Ways High Earners Commonly Get Burned

Stock compensation itself isn’t the problem. The problem is assuming it’s simpler than it actually is.

- Assuming Taxes Were Already Handled

A vesting event occurs, taxes are withheld, and everything seems taken care of. But withholding doesn’t always align with an individual’s actual marginal tax rate — especially for higher earners. If income is already elevated, supplemental withholding may fall short. And when multiple stock compensation events occur throughout the year, that shortfall can quietly compound into a larger-than-expected tax bill at filing time.

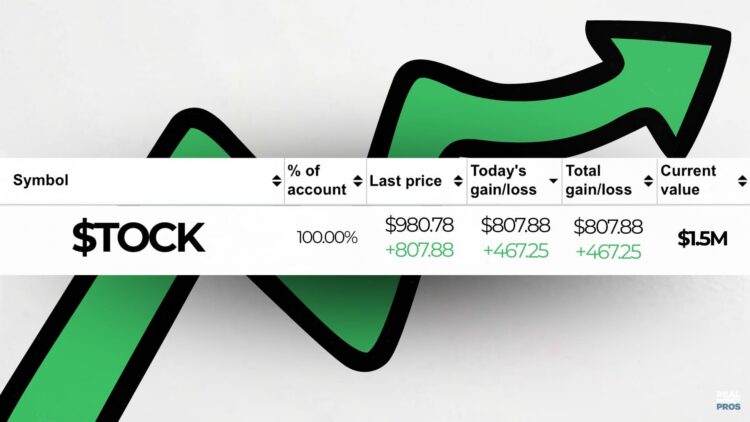

- Letting Employer Stock Become Too Large a Share of Net Worth

When employer stock performs well, it becomes easy to justify holding more. You know the company. You believe in the leadership. The stock has worked. Selling can feel emotionally difficult, even disloyal.

That’s understandable — but concentration risk doesn’t care about familiarity or loyalty. At some point, what helped build wealth can become its biggest threat.

- Making Timing Decisions Without a Tax Strategy

Stock compensation creates choices: When should you sell? Should you hold for more favorable treatment? When does exercising make sense? Without a plan, these decisions tend to become reactive. And what looks like a straightforward move can create ripple effects across your broader financial picture — affecting tax brackets, capital gains exposure, estimated payments, Medicare premium surcharges, and cash flow flexibility. Timing matters far more than most people realize.

- Treating Stock Compensation as an Isolated Decision

This may be the most overlooked issue of all. Stock compensation rarely lives in a vacuum. It intersects with tax planning, diversification, retirement strategy, charitable opportunities, and overall cash flow. That’s why the real question usually isn’t “Should I sell?” — it’s “How does this fit into the rest of the plan?”

Why This Gets Complicated Fast

Part of the confusion is that people tend to group all stock compensation together. But these structures behave very differently.

RSUs are generally taxed as ordinary income when shares vest — meaning you may owe taxes even if you don’t sell a single share.

Stock options vary in tax treatment depending on how they’re structured and when you act. Exercise decisions matter. Sale timing matters. Mistakes here can be costly.

ESPPs can be genuinely valuable, but holding periods and sale timing can materially shift the tax outcome. The details matter — a lot.

This is exactly why assumptions create problems.

What Better Planning Actually Looks Like

This doesn’t mean every executive needs an elaborate strategy. But it does mean stock compensation deserves intentional attention.

Depending on your situation, the right conversations might include evaluating whether withholding is adequate, coordinating sale timing more deliberately, reducing concentrated employer stock exposure over time, or integrating equity decisions into broader tax and retirement planning. Charitable strategies may also come into play.

The goal isn’t complexity for its own sake. It’s avoiding avoidable, expensive mistakes.

Final Thought

Equity compensation can be a remarkable wealth-building tool. But complexity tends to scale right alongside the opportunity.

The issue is rarely the stock itself. It’s the lack of coordination around how that compensation fits into the bigger financial picture. For many high earners, the biggest surprise isn’t receiving equity. It’s discovering too late that no one was really planning around it.

If your stock compensation has grown into a meaningful part of your financial life, it may be worth a conversation!

Use our “Find an Advisor” tab to get connected with our team and we’ll pair you with an advisor who’s best suited to help you.